PRAGMATRADING.COM1P R A G M A R E S E A R C H NOTE

TCA IS STRAI G H T F O R WA R D I N

THEORY BUT H A R D I N P R A C T I C E

The good practice of randomized trading experi-

ments is becoming more widely used, as seen

in the growing use of “wheels.” But traders still

face a big challenge when trying to decide which

of several different execution methods is better

because of a wide variety of confounding factors

and limited data set size available to most traders.

SO WHAT?

The risk is that traders make decisions based on

noise, and get worse outcomes for their investors.

This research note explores some real-world challenges,

and suggests best practices to develop confidence in

such comparisons given those challenges.

THE DATA SE T

To illustrate the challenges in a “controlled environ-

ment,” we work with a proprietary data set of 45,000

actual VWAP market orders traded in Q2-Q3 of 2020.

We use real orders because many of the challenges

in TCA result from the fat-tailed distribution of order

characteristics and performance results in real trading

data sets, and VWAP is a commonly used algorithm

by firms who quantitatively track execution shortfall.

VWAP SF NUM. OF

ORDERS

NOTIONAL

VALUE

SPREAD QTY /

ADV

AVG.

DURATION

1.26 bps 45,000 $24B 6.6 bps 0.8% 5 hours

TA B L E 1

Data summary with value-weighted performance.

NO. 25 | NOVEMBER 2 0 2 0

Measuring Execution Quality —

Finding the Signal in the Noise

A S I N G L E S I M U L AT E D

T R A D I N G E X P E R I M E N T

We simulate a typical trader’s “experiment.”

The trader has 400 parent orders per day to work

with, split across two algos, A and B, and reviews

performance after a 3 month period.

We simulate this experiment by choosing a random

3 month interval from our data set. To mimic a trader

splitting the day’s basket among algos, for each day in

the interval, we randomly assign each order to either

group A or group B with a coin toss. Of course, since

the same algo traded all the orders and the groups

were randomly assigned, groups A and B have the

same underlying performance. To simulate the situa-

tion where there are actually two different algos used,

one better than the other, we simply improve the

average price of each order in group A by 5% of

the spread, or about 0.3 bps on average. This creates

two different performance results, one for each algo.

Because we’re simply improving the average price

for the A group, we expect to improve its shortfall

regardless of what benchmark we decide to use.

The resulting data set for one such experiment

looks like this:

GROUP VWAP SF NUM. OF

ORDERS

NOTIONAL

VALUE

SPREAD QTY /

ADV

AVG.

DURATION

A –

Better

Algo

1.28 bps

(worse SF)

11,500 $6.4B 6.4 bps 0.86 % 5 hours

B –

Worse

Algo

1.21 bps

(better SF)

11,550 $6.9B 6.3 bps 0.88 % 5 hours

TABLE 2

Value-weighted performance summary of a single A/B experiment

over 3 months of data.

TCA IS STRAI G H T F O R WA R D I N

THEORY BUT H A R D I N P R A C T I C E

The good practice of randomized trading experi-

ments is becoming more widely used, as seen

in the growing use of “wheels.” But traders still

face a big challenge when trying to decide which

of several different execution methods is better

because of a wide variety of confounding factors

and limited data set size available to most traders.

SO WHAT?

The risk is that traders make decisions based on

noise, and get worse outcomes for their investors.

This research note explores some real-world challenges,

and suggests best practices to develop confidence in

such comparisons given those challenges.

THE DATA SE T

To illustrate the challenges in a “controlled environ-

ment,” we work with a proprietary data set of 45,000

actual VWAP market orders traded in Q2-Q3 of 2020.

We use real orders because many of the challenges

in TCA result from the fat-tailed distribution of order

characteristics and performance results in real trading

data sets, and VWAP is a commonly used algorithm

by firms who quantitatively track execution shortfall.

VWAP SF NUM. OF

ORDERS

NOTIONAL

VALUE

SPREAD QTY /

ADV

AVG.

DURATION

1.26 bps 45,000 $24B 6.6 bps 0.8% 5 hours

TA B L E 1

Data summary with value-weighted performance.

NO. 25 | NOVEMBER 2 0 2 0

Measuring Execution Quality —

Finding the Signal in the Noise

A S I N G L E S I M U L AT E D

T R A D I N G E X P E R I M E N T

We simulate a typical trader’s “experiment.”

The trader has 400 parent orders per day to work

with, split across two algos, A and B, and reviews

performance after a 3 month period.

We simulate this experiment by choosing a random

3 month interval from our data set. To mimic a trader

splitting the day’s basket among algos, for each day in

the interval, we randomly assign each order to either

group A or group B with a coin toss. Of course, since

the same algo traded all the orders and the groups

were randomly assigned, groups A and B have the

same underlying performance. To simulate the situa-

tion where there are actually two different algos used,

one better than the other, we simply improve the

average price of each order in group A by 5% of

the spread, or about 0.3 bps on average. This creates

two different performance results, one for each algo.

Because we’re simply improving the average price

for the A group, we expect to improve its shortfall

regardless of what benchmark we decide to use.

The resulting data set for one such experiment

looks like this:

GROUP VWAP SF NUM. OF

ORDERS

NOTIONAL

VALUE

SPREAD QTY /

ADV

AVG.

DURATION

A –

Better

Algo

1.28 bps

(worse SF)

11,500 $6.4B 6.4 bps 0.86 % 5 hours

B –

Worse

Algo

1.21 bps

(better SF)

11,550 $6.9B 6.3 bps 0.88 % 5 hours

TABLE 2

Value-weighted performance summary of a single A/B experiment

over 3 months of data.

PRAGMATRADING.COM2N O V EM B E R 2 0 2 0

-20 -10 0 10 20

0

10

20

30

40

50

-2 -1 0 1 2

A looks better B looks better A looks better B looks better

0

25

50

75

100

125

C O U N T

S F D I F F E R E N C E ( B P S )

Arrival Price SF (bps) VWAP SF (bps)

SF DIFFERENCE (BPS)

Wrong

49%

Wrong

32%

TRUE PERFORMANCE BENEFIT OF A OVER B NO PERFORMANCE BENEFIT

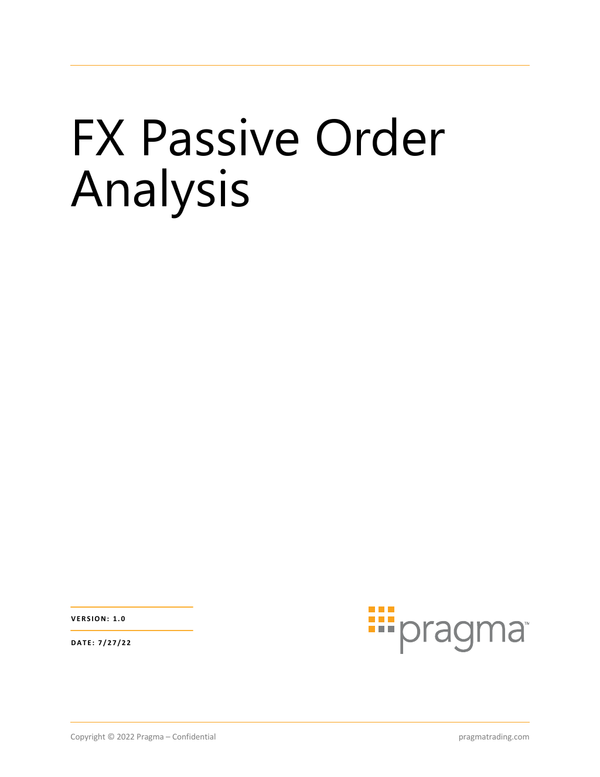

F I G U R E 1

This figure shows a histogram of the difference between the average shortfall of algos A and B. Each point represents a single experiment

as described above, and the histogram shows the distribution of how often each outcome is seen when we repeat the experiment 500

times. Negative values mean that A was observed to be better than B (lower shortfall, the reality), 0 means they’re observed to be the

same, and positive means B was seen to be better than A.

In this particular experiment, algo B looks slightly

better—the opposite of the reality. After 3 months of

experiment, splitting flow cleanly across two algos, we

still got the wrong answer! But is this just an anomaly?

REPEATED RA N D O M S A M P L E S

Although in real life a trader only gets to see one

outcome of such an experiment, we can simulate the

random split of orders between two algos as many

times as we want, and we do so 500 times to get a

sense for how reliable such an experiment is. What

we’d hope is that we consistently see A outperforming

B, with perhaps a few anomalous cases where we got

the wrong answer. The histogram below shows each

such 3-month experiment as a single data point, and

the count of these outcomes bucketed by relative

outperformance of A over B (negative is good,

because lower shortfall). We illustrate the results both

in terms of VWAP shortfall and Arrival Price shortfall.

Note the “true” value (A is better than B by about

0.3 bps) is shown by the green line. We see that

for VWAP shortfall, the distribution of outcomes

is centered around that true value. Yet 1/3 of the

time, even this rigorously randomized 3-month

long experiment will give the wrong answer, shown

by the orange bars to the right of the dotted line,

and we’ll think that B is actually better than A.

Though for many traders Arrival Price slip-

page, shown in the left plot, is the true “gold

standard” performance metric, it’s a much

noisier metric.1 As we see below, measuring by

Arrival Price shortfall correctly identifies A as the

better algo only 51% of the time, barely more

than a random flip of a coin, and erroneously

crowns algo B as the winner 49% of the time!

1 For full-day orders, Arrival Price slippage varies by on

the order of the stock’s daily price change, since there is a

single point-in-time benchmark at the start, and trading occurs

throughout the day. In contrast, VWAP is effectively a rolling

average of prices calculated across the period of the trade,

so tends to deviate less from actual average price of an algo

that also spreads its trading out across the same period.

-20 -10 0 10 20

0

10

20

30

40

50

-2 -1 0 1 2

A looks better B looks better A looks better B looks better

0

25

50

75

100

125

C O U N T

S F D I F F E R E N C E ( B P S )

Arrival Price SF (bps) VWAP SF (bps)

SF DIFFERENCE (BPS)

Wrong

49%

Wrong

32%

TRUE PERFORMANCE BENEFIT OF A OVER B NO PERFORMANCE BENEFIT

F I G U R E 1

This figure shows a histogram of the difference between the average shortfall of algos A and B. Each point represents a single experiment

as described above, and the histogram shows the distribution of how often each outcome is seen when we repeat the experiment 500

times. Negative values mean that A was observed to be better than B (lower shortfall, the reality), 0 means they’re observed to be the

same, and positive means B was seen to be better than A.

In this particular experiment, algo B looks slightly

better—the opposite of the reality. After 3 months of

experiment, splitting flow cleanly across two algos, we

still got the wrong answer! But is this just an anomaly?

REPEATED RA N D O M S A M P L E S

Although in real life a trader only gets to see one

outcome of such an experiment, we can simulate the

random split of orders between two algos as many

times as we want, and we do so 500 times to get a

sense for how reliable such an experiment is. What

we’d hope is that we consistently see A outperforming

B, with perhaps a few anomalous cases where we got

the wrong answer. The histogram below shows each

such 3-month experiment as a single data point, and

the count of these outcomes bucketed by relative

outperformance of A over B (negative is good,

because lower shortfall). We illustrate the results both

in terms of VWAP shortfall and Arrival Price shortfall.

Note the “true” value (A is better than B by about

0.3 bps) is shown by the green line. We see that

for VWAP shortfall, the distribution of outcomes

is centered around that true value. Yet 1/3 of the

time, even this rigorously randomized 3-month

long experiment will give the wrong answer, shown

by the orange bars to the right of the dotted line,

and we’ll think that B is actually better than A.

Though for many traders Arrival Price slip-

page, shown in the left plot, is the true “gold

standard” performance metric, it’s a much

noisier metric.1 As we see below, measuring by

Arrival Price shortfall correctly identifies A as the

better algo only 51% of the time, barely more

than a random flip of a coin, and erroneously

crowns algo B as the winner 49% of the time!

1 For full-day orders, Arrival Price slippage varies by on

the order of the stock’s daily price change, since there is a

single point-in-time benchmark at the start, and trading occurs

throughout the day. In contrast, VWAP is effectively a rolling

average of prices calculated across the period of the trade,

so tends to deviate less from actual average price of an algo

that also spreads its trading out across the same period.

")