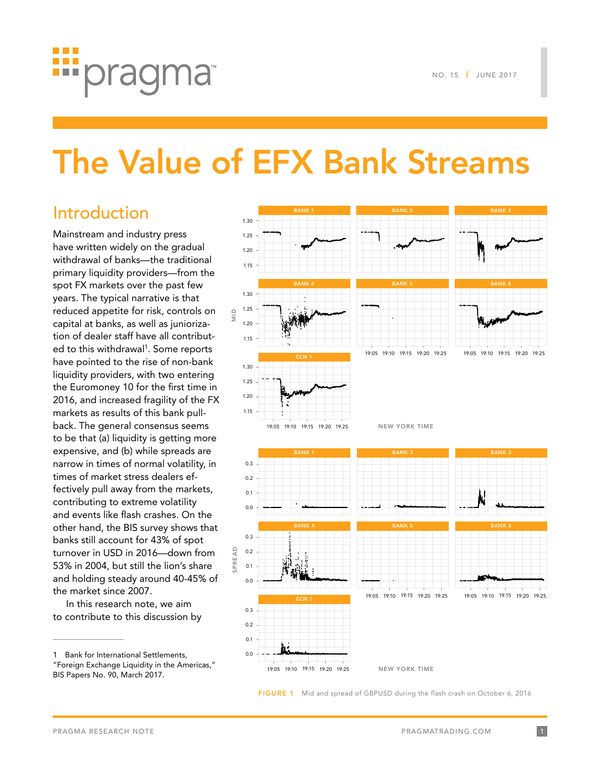

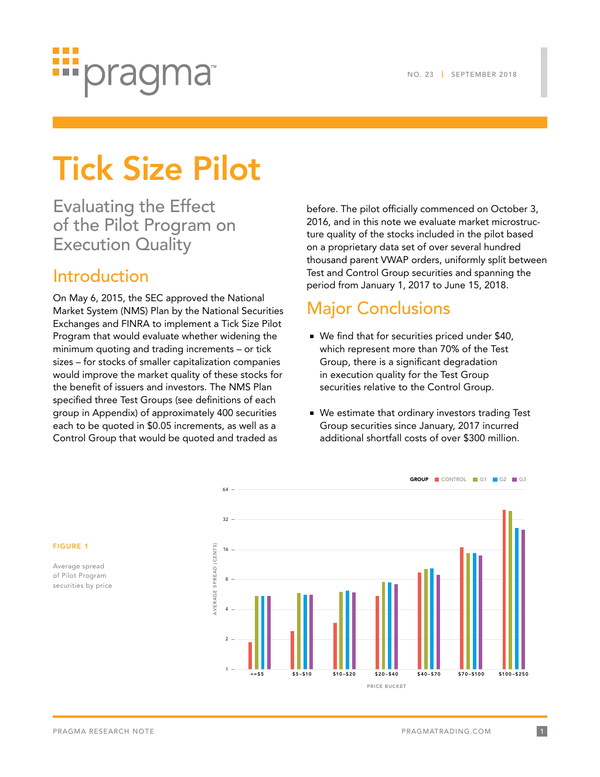

PRAGMATRADING.COM1P R A G M A R E S E A R C H NOTE

Traders on both the buy-side and sell-side focus

much attention and energy on trading venues and

order types. There is a notion, implicitly encouraged

by many trading venues, that best execution can be

achieved through venue curation—routing to good

venues and shunning bad ones. But the reality is more

complex: venues offer tradeoffs, and best execution

can only be achieved by using venues and order types

selectively and intelligently, based on stock character-

istics, order characteristics, and dynamic signals.

In competing for order flow, trading venues tend

toward simplistic marketing claims to imply that

their venue or order type is better than others.

Displayed venues often tout their volumes and fill

rates. Dark venues and hidden or discretionary

order type pitches often focus on fill quality, usually

measured by markout. Block-oriented venues talk

NO. 26 | OCTOBER 202 1

On the Limits of Markouts

and Venue Curation

about trade size. The reality is that venues and

order types offer tradeoffs between execution

quality and fill rate. There is no best venue or

order type that should be used across all stock

characteristics, trading goals, and market conditions.

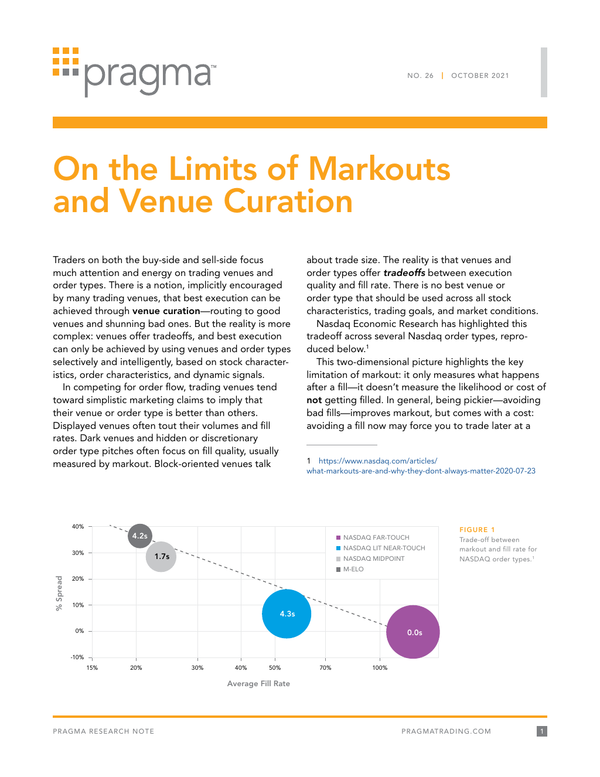

Nasdaq Economic Research has highlighted this

tradeoff across several Nasdaq order types, repro-

duced below.1

This two-dimensional picture highlights the key

limitation of markout: it only measures what happens

after a fill—it doesn’t measure the likelihood or cost of

not getting filled. In general, being pickier—avoiding

bad fills—improves markout, but comes with a cost:

avoiding a fill now may force you to trade later at a

1 https://www.nasdaq.com/articles/

what-markouts-are-and-why-they-dont-always-matter-2020-07-23

15% 20% 30% 40% 50% 70% 100%

-10%

0%

10%

20%

30%

40%

Average Fill Rate

% Spread

4.2s

1.7s

4.3s

0.0s

NASDAQ FAR-TOUCH

NASDAQ LIT NEAR-TOUCH

NASDAQ MIDPOINT

M-ELO

FIGURE 1

Trade-off between

markout and fill rate for

NASDAQ order types.1

Traders on both the buy-side and sell-side focus

much attention and energy on trading venues and

order types. There is a notion, implicitly encouraged

by many trading venues, that best execution can be

achieved through venue curation—routing to good

venues and shunning bad ones. But the reality is more

complex: venues offer tradeoffs, and best execution

can only be achieved by using venues and order types

selectively and intelligently, based on stock character-

istics, order characteristics, and dynamic signals.

In competing for order flow, trading venues tend

toward simplistic marketing claims to imply that

their venue or order type is better than others.

Displayed venues often tout their volumes and fill

rates. Dark venues and hidden or discretionary

order type pitches often focus on fill quality, usually

measured by markout. Block-oriented venues talk

NO. 26 | OCTOBER 202 1

On the Limits of Markouts

and Venue Curation

about trade size. The reality is that venues and

order types offer tradeoffs between execution

quality and fill rate. There is no best venue or

order type that should be used across all stock

characteristics, trading goals, and market conditions.

Nasdaq Economic Research has highlighted this

tradeoff across several Nasdaq order types, repro-

duced below.1

This two-dimensional picture highlights the key

limitation of markout: it only measures what happens

after a fill—it doesn’t measure the likelihood or cost of

not getting filled. In general, being pickier—avoiding

bad fills—improves markout, but comes with a cost:

avoiding a fill now may force you to trade later at a

1 https://www.nasdaq.com/articles/

what-markouts-are-and-why-they-dont-always-matter-2020-07-23

15% 20% 30% 40% 50% 70% 100%

-10%

0%

10%

20%

30%

40%

Average Fill Rate

% Spread

4.2s

1.7s

4.3s

0.0s

NASDAQ FAR-TOUCH

NASDAQ LIT NEAR-TOUCH

NASDAQ MIDPOINT

M-ELO

FIGURE 1

Trade-off between

markout and fill rate for

NASDAQ order types.1

PRAGMATRADING.COM2O C T O B E R 2 0 2 1

worse price—whether to stay on a VWAP schedule

dictated by the trader, or just to eventually complete

the order. This isn’t rocket science—most traders are

familiar with these tradeoffs in the context of using

optimistic limit prices, where the benefit of holding

out for a better price has to be weighed against the

risk you might “miss the market.”

It’s generally the balance of these two competing

effects, and whether they match the specific trading

situation, that determine whether a venue or tactic is

good or bad. Using a picky order type when trading

an urgent order can degrade performance. Simple use

of markout does not show this obvious fact.

A Markout Case Study:

IEX D-Limit

Last fall IEX introduced the D-Limit order type, con-

tinuing their track record of innovation. Simply put,

D-Limit orders are designed to pull from the market

and avoid execution when it looks like the market is

likely to trade through them. This is a reasonable idea:

avoiding being run over is generally a good thing. IEX

posted a blog highlighting this benefit by showing

that D-Limit orders have better markout than other

venues’ ordinary passive orders.2

This is fine as far as it goes, but common sense tells

us that IEX’s D-Limit might come at some opportunity

cost in missed liquidity—not just because of the order

pulling, but also because IEX as a venue only repre-

sents about 3% of market volume, most of it at mid-

point, and without the large rebate to attract takers as

2 https://medium.com/boxes-and-lines/d-limit-one-of-these-

things-is-not-like-the-others-3c6b438d3a6e

some inverted venues have. If those opportunity costs

are too high, use of this “smart” order type could hurt

performance.

IEX followed up with another blog to answer this ques-

tion, as they put it “are D-Limit’s performance and price

improvement worth its lower fill rate?”3 Unfortunately

there were two big limitations in their analysis.

The first problem is that D-Limit was compared not

against posting a limit order on say Nasdaq or NYSE,

but posting a standard limit order on IEX. This leaves

the possibility that while IEX D-Limit is preferable to

a regular IEX limit order, it is still inferior to options

available on other venues with a higher probability

of fill. This is a serious problem because the market

running away before you get filled is exactly the kind

of opportunity cost you should worry about when

posting a picky order on a small venue.

The second problem is the analysis looked only at

D-Limit orders that were pulled and where the market

then didn’t tick up above the original limit price within a

second. But this leaves out many possible bad outcomes

of posting an order, including all the cases where the

order wasn’t executed and the market ticked away to

above the original posting price. A proper accounting

of the cost of any trading tactic must be a probability-

weighted average of all the possible outcomes—the bad

as well as the good. IEX presumably reasoned that such

bad outcomes would be equal between regular IEX

and IEX D-Limit orders—but this returns us to the first

problem: how many bad outcomes are there when post-

ing IEX D-Limit vs. say posting a regular limit order on

Nasdaq, and how do these weigh against the benefits?

3 https://medium.com/boxes-and-lines/d-limit-performance-the-

fill-rates-race-4dcd26661a98

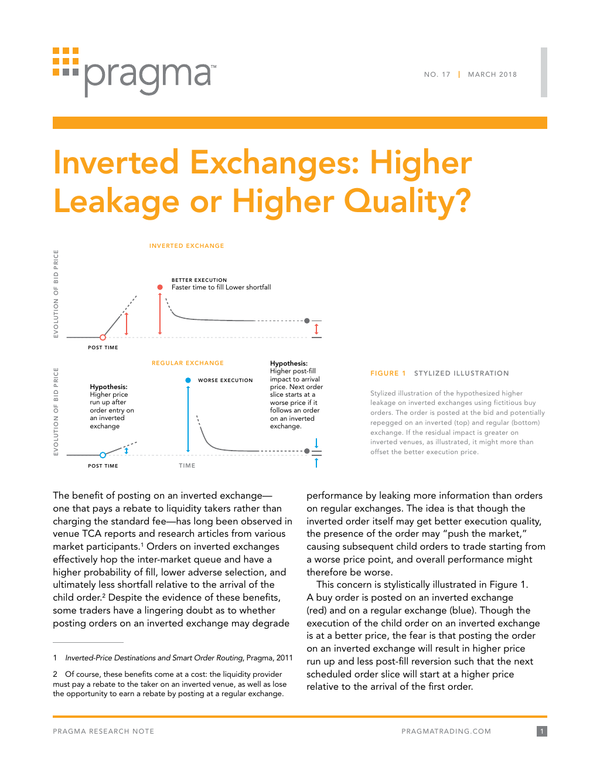

10 20 30 40 50

Fill Rate (%)

40

30

50

Markout – % Spread

IEX D-LIMIT

IEX

STANDARD

INVERTED

BETTER PERFORMANCE

FIGURE 2

Markout and Fill Rate of

Near-Touch Limit Orders

Markout and fill rate of IEX regular limit and

IEX D-Limit vs. regular limit orders on two

of the largest maker-taker (Standard) and

taker-maker (Inverted) exchanges. Markouts

are measured 1 second after execution relative

to the far touch and include fees. D-Limit

appears to have better markout but lower

probability of fill. This doesn’t tell us anything

definitive about D-Limit, but illustrates

the first problem with the IEX analysis.

worse price—whether to stay on a VWAP schedule

dictated by the trader, or just to eventually complete

the order. This isn’t rocket science—most traders are

familiar with these tradeoffs in the context of using

optimistic limit prices, where the benefit of holding

out for a better price has to be weighed against the

risk you might “miss the market.”

It’s generally the balance of these two competing

effects, and whether they match the specific trading

situation, that determine whether a venue or tactic is

good or bad. Using a picky order type when trading

an urgent order can degrade performance. Simple use

of markout does not show this obvious fact.

A Markout Case Study:

IEX D-Limit

Last fall IEX introduced the D-Limit order type, con-

tinuing their track record of innovation. Simply put,

D-Limit orders are designed to pull from the market

and avoid execution when it looks like the market is

likely to trade through them. This is a reasonable idea:

avoiding being run over is generally a good thing. IEX

posted a blog highlighting this benefit by showing

that D-Limit orders have better markout than other

venues’ ordinary passive orders.2

This is fine as far as it goes, but common sense tells

us that IEX’s D-Limit might come at some opportunity

cost in missed liquidity—not just because of the order

pulling, but also because IEX as a venue only repre-

sents about 3% of market volume, most of it at mid-

point, and without the large rebate to attract takers as

2 https://medium.com/boxes-and-lines/d-limit-one-of-these-

things-is-not-like-the-others-3c6b438d3a6e

some inverted venues have. If those opportunity costs

are too high, use of this “smart” order type could hurt

performance.

IEX followed up with another blog to answer this ques-

tion, as they put it “are D-Limit’s performance and price

improvement worth its lower fill rate?”3 Unfortunately

there were two big limitations in their analysis.

The first problem is that D-Limit was compared not

against posting a limit order on say Nasdaq or NYSE,

but posting a standard limit order on IEX. This leaves

the possibility that while IEX D-Limit is preferable to

a regular IEX limit order, it is still inferior to options

available on other venues with a higher probability

of fill. This is a serious problem because the market

running away before you get filled is exactly the kind

of opportunity cost you should worry about when

posting a picky order on a small venue.

The second problem is the analysis looked only at

D-Limit orders that were pulled and where the market

then didn’t tick up above the original limit price within a

second. But this leaves out many possible bad outcomes

of posting an order, including all the cases where the

order wasn’t executed and the market ticked away to

above the original posting price. A proper accounting

of the cost of any trading tactic must be a probability-

weighted average of all the possible outcomes—the bad

as well as the good. IEX presumably reasoned that such

bad outcomes would be equal between regular IEX

and IEX D-Limit orders—but this returns us to the first

problem: how many bad outcomes are there when post-

ing IEX D-Limit vs. say posting a regular limit order on

Nasdaq, and how do these weigh against the benefits?

3 https://medium.com/boxes-and-lines/d-limit-performance-the-

fill-rates-race-4dcd26661a98

10 20 30 40 50

Fill Rate (%)

40

30

50

Markout – % Spread

IEX D-LIMIT

IEX

STANDARD

INVERTED

BETTER PERFORMANCE

FIGURE 2

Markout and Fill Rate of

Near-Touch Limit Orders

Markout and fill rate of IEX regular limit and

IEX D-Limit vs. regular limit orders on two

of the largest maker-taker (Standard) and

taker-maker (Inverted) exchanges. Markouts

are measured 1 second after execution relative

to the far touch and include fees. D-Limit

appears to have better markout but lower

probability of fill. This doesn’t tell us anything

definitive about D-Limit, but illustrates

the first problem with the IEX analysis.